What Happens During Recessions,

Crunches and Busts?

Stijn Claessens, M. Ayhan Kose, and Marco E. Terrones

WP/08/274

© 2008 International Monetary Fund WP/08/274

IMF Working Paper

Research Department

What Happens During Recessions, Crunches and Busts?

Prepared by Stijn Claessens, M. Ayhan Kose and Marco E. Terrones

1

December 2008

Abstract

This Working Paper should not be reported as representing the views of the IMF.

The views expressed in this Working Paper are those of the author(s) and do not necessarily represent

those of the IMF or IMF policy. Working Papers describe research in progress by the author(s) and are

published to elicit comments and to further debate.

We provide a comprehensive empirical characterization of the linkages between key

macroeconomic and financial variables around business and financial cycles for 21 OECD

countries over the period 1960–2007. In particular, we analyze the implications of 122

recessions, 112 (28) credit contraction (crunch) episodes, 114 (28) episodes of house price

declines (busts), 234 (58) episodes of equity price declines (busts) and their various overlaps

in these countries over the sample period. Our results indicate that interactions between

macroeconomic and financial variables can play major roles in determining the severity and

duration of recessions. Specifically, we find evidence that recessions associated with credit

crunches and house price busts tend to be deeper and longer than other recessions.

JEL Classification Numbers: E32; E44; E51; F42

Keywords: Business cycles, recessions, credit crunches, house prices, equity prices, busts

Author’s E-Mail Address: scl[email protected]; akose@imf.org; [email protected]

1

We are grateful for helpful comments from Lewis Alexander, Michael Dooley, Kristin Forbes,

Prakash Loungani, and our discussants, Steven Kamin, Desmond Lachman, Vincent Reinhart, and

Angel Ubide, and participants at various seminars and conferences where earlier versions of this

paper were presented. Dio Kaltis, David Low, Yongjoon Shin and Zhi (George) Yu provided

excellent research assistance.

2

Contents Page

Executive Summary...................................................................................................................4

Figure A. What Happens During Recessions: Crunches and Busts? ........................................6

I. Introduction ............................................................................................................................7

II. Database and Methodology.................................................................................................10

A. Database..................................................................................................................10

B. Methodology ...........................................................................................................11

III. What Happens During Recessions?...................................................................................14

A. Basic Features of Recessions: Duration and Cost...................................................14

B. Changes in Macroeconomic and Financial Variables.............................................16

C. Dynamics of Recessions..........................................................................................17

D. Synchronization of Recessions, Credit Contractions and Asset Price Declines.....18

IV. What Happens During Credit Contractions and Asset Price Declines? ............................20

A. Episodes of Credit Contractions .............................................................................20

B. Episodes of Declines in House Prices.....................................................................22

C. Episodes of Declines in Equity Prices.....................................................................23

D. Credit Contractions and Asset Price Declines: A Summary...................................24

V. What Happens During Recessions Associated with Crunches and Busts?.........................24

A. Recessions Associated with Credit Crunches .........................................................25

B. Recessions Associated with House Price Busts ......................................................25

C. Recessions Associated with Equity Price Busts......................................................26

D. Recessions Associated with Crunches and Busts: A Summary..............................27

VI. Recessions Associated with Increases in Oil Prices ..........................................................28

VII. Policy Responses During Recessions, Crunches and Busts.............................................29

VIII. Recession Outcomes and Financial Factors....................................................................30

IX. Conclusion.........................................................................................................................34

A. A Summary .............................................................................................................34

B. Lessons for Today ...................................................................................................34

C. Caveats and Future Research ..................................................................................35

References................................................................................................................................36

Figures

1. Associations Between Recessions, Crunches and Busts......................................................43

2. Recessions: Duration and Amplitude...................................................................................44

3. Recessions in OECD Countries ...........................................................................................45

4. Synchronization of Recessions ............................................................................................48

5. Synchronization of Credit Contractions and Asset Price Declines......................................49

3

6. Credit Crunches in OECD Countries...................................................................................50

7. House Price Busts in OECD Countries................................................................................52

8. Equity Price Busts in OECD Countries ...............................................................................54

Tables

1A. Recessions: Summary Statistics........................................................................................56

1B. Recessions: Summary Statistics........................................................................................57

2A. Credit Contractions: Basic Statistics.................................................................................58

2B. Credit Contractions: Basic Statistics.................................................................................59

3A. House Price Declines: Basic Statistics..............................................................................60

3B. House Price Declines: Basic Statistics..............................................................................61

4A. Equity Price Declines: Basic Statistics .............................................................................62

4B. Equity Price Declines: Basic Statistics..............................................................................63

5. Credit Contractons and Asset Price Declines: Summary Statistics ...................................64

6. Leads and Lags: Recessions, Crunches and Busts............................................................65

7. Recessions Associated with Credit Crunches...................................................................66

8. Recessions Associated with House Price Busts ...............................................................67

9. Recessions Associated with Equity Price Busts ...............................................................68

10. Recessions Associated with Crunches and Busts: Summary Statistics ............................69

11. Recessions Associated with Oil Price Shocks ..................................................................70

12. Changes in Poicy Variables ..............................................................................................71

13A.Cost of Recessions ...........................................................................................................72

13B.Cost of Recessions ...........................................................................................................73

14A.Cost of Recessions ...........................................................................................................74

14B.Cost of Recessions ...........................................................................................................75

Appendix: Database ................................................................................................................41

4

Executive Summary

The current financial turmoil that started in the United States, initially led by sharp declines

in house prices, has transformed into a severe credit crunch with substantial losses in equity

markets. Moreover, it has now spread to a number of advanced and emerging countries, and

become the most severe global financial crisis since the Great Depression. This has led to an

intensive debate about how much the crisis will impact the real economy. There are already

indications that the spillovers from the difficulties in financial sector to economic activity

will not be mild — in fact, activity in the United States and several other advanced

economies has been contracting in recent months.

These developments have highlighted a number of questions about the linkages between the

financial sector and the real economy during recessions. Two specific questions that have

often been raised in the context of this debate are: How do macroeconomic and financial

variables behave around recessions, credit crunches and asset (house and equity) price busts?

And are recessions associated with credit crunches and asset price busts different than other

recessions?

In order to address these questions, we provide a comprehensive empirical characterization

of the linkages between key macroeconomic and financial variables around business and

financial cycles for 21 OECD countries over the 1960-2007 period. In particular, we analyze

the implications of 122 recessions, 112 (28) credit contraction (crunch) episodes, 114 (28)

episodes of house price declines (busts), and 234 (58) episodes of equity price declines

(busts) in these countries over the sample period, their implications and various overlaps. The

main results are as follows:

• The typical recession lasts almost 4 quarters and is associated with an output drop of

roughly 2 percent (Figure A). Most macroeconomic and financial variables exhibit

procyclical behavior during recessions. While recessions have been becoming shorter and

milder over time, they remain highly synchronized across countries. Moreover, recessions

often coincide with the episodes of contractions in domestic credit and declines in asset

prices.

• Episodes of credit crunches, house price and equity price busts last much longer than

recessions do. For example, a credit crunch episode typically lasts two-and-a-half years and

is associated with nearly a 20 percent decline in credit. A housing bust tends to persist even

longer—four-and-a-half years with a 30 percent fall in real house prices. And an equity price

bust lasts some 10 quarters and when it is over, the real value of equities drops by half.

• In one out of six recessions, there is also a credit crunch underway, and in one out of

four recessions a house price bust. Equity price busts coincide with one-third of recession

episodes. There can be considerable lags between financial market disturbances and real

activity. A recession, if one occurs, can start as late as four to five quarters after the onset of a

credit crunch or housing bust.

5

• Most importantly, recessions associated with credit crunches and house price busts

are deeper and last longer than other recessions do. In particular, although recessions

accompanied with severe credit crunches or house price busts last only three months longer,

they typically result in output losses two to three times greater than recessions without such

financial stresses. There is also evidence that the extent of declines in house prices appears to

influence the depth of recessions, even after accounting for the changes in other financial

variables, including credit and equity prices, and various other controls. These findings

suggest that the strength of linkages between the financial sector and the real economy can

aggravate output losses during recessions.

• The lessons from the earlier episodes of recessions, crunches and busts we examined

are sobering, suggesting that recessions following the current crisis will likely be more costly

than other recessions because they take place alongside simultaneous credit crunches and

asset price busts. Furthermore, although the effects of the current crisis have already been felt

around the world, the past evidence suggests that its global dimensions are likely to intensify

in the coming months.

6

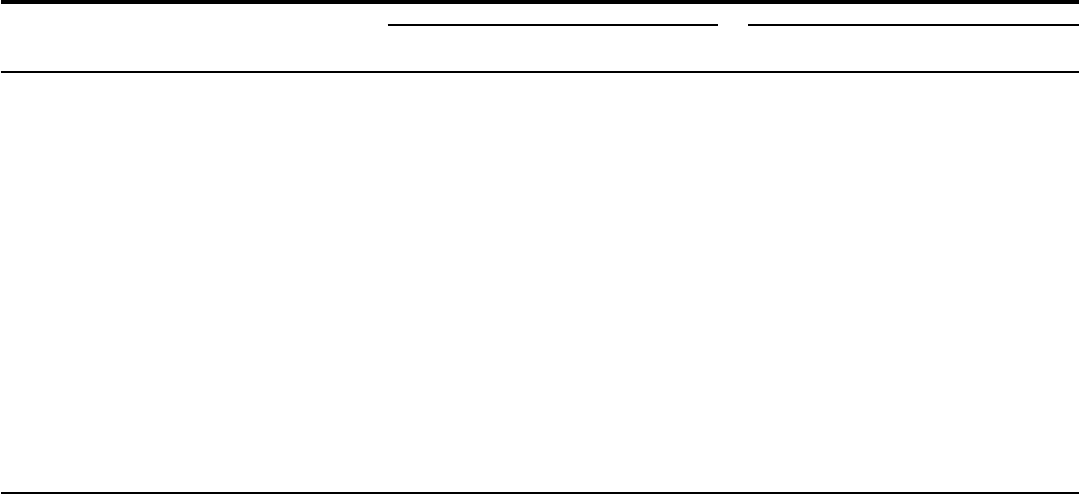

Figure A. What Happens During Recessions, Crunches and Busts?

-6

-4

-2

0

2

4

6

All Recessions

Severe Recessions

GDP Growth

(in percent)

Duration

(Number of Quarters)

R

ecessions can be long and deep...

0

20

40

60

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

GDP

Credit

fraction of countries in recession/credit contraction,

in percent

-8

-6

-4

-2

0

Without a Crunch/Bust

With a Crunch/Bust

With a Severe Crunch/Bust

Credit Crunch

(GDP Loss, in percent)

House Price Bust

(GDP Loss, in percent)

Credit-crunch and house-price-bust recessions

are usually deeper

-40

-30

-20

-10

0

10

20

30

Credit Crunch

House Price Bust

Duration

(Number of Quarters)

Credit/House Price

Growth

(in percent)

Crunches and busts are typically long with

s

ubstantial declines in credit and house price

… and highly synchronized across countries and

often coincide with credit contractions

Notes: GDP growth is the percent change in the level of output during the recession period. Severe

recessions refer to those in which the peak-to-trough decline in output is in the top quartile of all

recession-related output declines. Synchronization is measured by the fraction of countries experiencing a

recession or a credit contraction at the same time. GDP loss is the total amount of GDP lost between the

peak and trough of a recession. Severe credit crunches and house price busts are those that are in the top

half of all crunch and bust episodes.

7

“… recessions that follow swings in asset prices are not necessarily longer, deeper,

and associated with a greater fall in output and investment than other recessions…”

Roger W. Ferguson, Vice Chairman of the Federal Reserve Board, January 2005

“If we do end up dating the recession as beginning at the

end of last year, it could be a very long

recession.”

Martin Feldstein, Member of the NBER Business Cycle Dating Committee, August 2008

I. I

NTRODUCTION

The financial turmoil that started in the United States last year has now spread to a number of

advanced and emerging countries and transformed into the most severe global financial crisis

since the Great Depression. This has led to an intensive debate about how much the financial

crisis will impact the broader economies. There are already indications that the spillovers

from the financial crisis to the real economy will not be mild—in fact, activity in the United

States and several other advanced economies has been contracting in recent months.

These developments have highlighted a number of questions about the linkages between the

real economy and the financial sector during recessions. Two specific questions that have

often been raised in the context of this debate are: How do macroeconomic and financial

variables behave around recessions, credit crunches and asset (house and equity) price busts?

And are recessions associated with credit crunches and asset price busts different than other

recessions? In order to address these questions, we provide a comprehensive empirical

characterization of the linkages between key macroeconomic and financial variables around

business and financial cycles for 21 OECD countries over the 1960-2007 period.

We first identify turning points in these variables using standard business cycle dating

methods. We document 122 recessions, 112 credit contractions, 114 house price declines,

and 234 equity price declines for these countries over the sample period. When recessions,

credit contractions, house price and equity price declines fall into the top quartiles of all

recessions, contractions and declines, we define them as severe recessions, credit crunches,

house price busts and equity price busts, respectively. We then analyze the characteristics of

these events—in terms of their duration and severity—and the behavior of major

macroeconomic and financial variables around the various cycles.

With respect to the first question, we find that the typical recession lasts almost 4 quarters

and is associated with an output drop (decline from peak to trough) of roughly 2 percent.

Severe recessions are, by construction, much more costly, with a median decline of about

5 percent, and last a quarter longer. While typical recessions tend to result in a cumulative

loss of around 3 percent, severe ones cost three times more. As one would expect, most

macroeconomic and financial variables exhibit procyclical behavior during recessions. In

addition, recessions are characterized by sharp declines in (residential) investment, industrial

production, imports, and housing and equity prices, modest declines in consumption and

exports, and some decrease in employment rates. Two key policy related variables—short-

term interest rates and fiscal expenditures—often behave countercyclical during recessions.

8

For some observers, the global nature of the current crisis has been unprecedented, as several

advanced economies have simultaneously experienced difficulties in their credit markets as

well as declines in their house and equity prices. However, these recent phenomena are not

unusual because historically recessions, crunches and busts often occur at the same time

across countries. Indeed, recessions in many advanced countries were bunched in four

periods over the past 40 years—the mid-70s, the early 80s, the early 90s and the early-

2000s—and often coincided with global shocks. Just as many countries experience

synchronized recessions, countries also go through simultaneous episodes of credit

contractions. Moreover, declines in house and equity prices tend to occur at the same time.

Our findings indicate that the episodes of credit crunches, house price and equity price busts

last much longer than recessions do. For example, the average duration of a credit crunch is

around 10 quarters while an asset price bust is usually even longer, with an average duration

of 18 (12) quarters in the case of house (equity) price busts. The dynamics of the main

components of domestic absorption around these events are similar to those observed during

recessions. A much larger decline in the growth rate of investment compared with that of

consumption is a feature of both recessions as well as credit crunches and house price busts.

In particular, episodes of credit crunch and house price bust are accompanied with large

declines in residential investment. There is also evidence that credit crunches and house price

busts are more costly than equity price busts, as equity price busts are less consistently

associated with real sector outcomes.

For the second question, we document the coincidence of recessions with credit crunches or

asset price busts. In about one out of six recessions, there is also a credit crunch underway

and, in about one out of four recessions, also a house price bust. Equity price busts overlap

for about one-third of recession episodes. A recession, if one occurs, can start as late as four

to five quarters after the onset of a credit crunch or an asset bust.

In terms of duration and severity, we find that recessions associated with housing busts and

credit crunches are both deeper and longer-lasting than other recessions are. Differences in

total output loss between events with severe crunches and busts and those without typically

amount to one percentage point, while the duration is more than one quarter longer in case of

a housing bust. In terms of the behavior of key macroeconomic and financial variables, we

find that residential investment tends to fall more sharply in recessions with housing busts

and in those with credit crunches than in other recessions. Unemployment rates increase

notably more in recessions with housing busts.

In addition to our event study of interactions among various macroeconomic and financial

variables during recessions accompanied with (or without) credit crunches or asset price

busts, we also conduct a more formal analysis of the depth of recessions and the special roles

played by changes in financial market conditions during these episodes. In particular, we

employ a basic regression framework to examine how the amplitude of a recession is

associated with changes in financial variables during recessions. Our results suggest that the

changes in house prices tend to be the financial variable most robustly associated with the

depth of recessions. Besides by its duration, the extent of decline in output is most influenced

by the state of the economy at the onset of the recession.

9

Our study contributes to a large body of research analyzing the roles played by financial

variables in explaining fluctuations in economic activity. Financial and macroeconomic

variables closely interact through wealth and substitution effects, and through the impact they

have on the balance sheets of firms and households (see, for instance, Blanchard and Fischer,

1989; and Obstfeld and Rogoff, 1999). In particular, asset prices can, by affecting household

wealth, influence consumption, and by altering a firm’s net worth and the market value of the

capital stock relative to its replacement value, influence investment. Perhaps more

importantly, the interactions between the financial sector and the real economy can be

amplified through the financial accelerator and related mechanisms. According to these

mechanisms, an increase in asset prices improves a firm’s (or household’s) net worth,

enhancing its capacities to borrow, invest and spend. This process can in turn lead to further

increases in asset prices and have general equilibrium effects.

2

Various empirical studies—both macro- and microeconomic—have been able to provide

evidence for these channels.

3

For example, there is a large empirical literature analyzing the

dynamics of business cycles, asset price fluctuations and credit cycles (Bernanke and Gertler,

1989; Borio, Furfine and Lowe, 2001). This literature, however, mainly analyzes the general

procyclicality of financial and macroeconomic variables, and less so how interactions

between financial and real economic variables vary during recessions, which is our focus.

We also contribute to a branch of the large literature on business cycles which aims to

identify the turning points in macroeconomic and financial variables using various

methodologies. The classical methodology of dating business cycles we use here finds its

roots in the pioneering work of Burns and Mitchell (1946) and has been widely used over the

years (Harding and Pagan, 2006). Morsink, Helbling, and Tokarick (2002), for example,

employ this methodology to analyze the main features of recessions and recoveries in a

number of OECD countries. Fewer studies have conducted cross-country analyses of cycles

in asset prices identified by this method.

4

One example is Helbling and Terrones (2003)

which examines the implications of asset price booms and busts in a large set of industrial

countries and conclude that house price busts are typically more costly than equity price

busts are.

Although the roles played by financial variables in business cycles have thus received much

attention from various theoretical and empirical perspectives, most of these studies have

considered the topics of business cycle, credit and asset prices independently (or in isolation).

Furthermore, the links between real and financial variables during recessions have yet to be

2

Some of the seminal models with these general equilibrium dynamics include Bernanke and Gertler

(1989) and Kiyotaki and Moore (1997) followed by extensions of these models that also have

dynamics which resemble Fisher’s (1933) debt-deflation mechanism. Mendoza (2008) uses this

framework to examine sudden stops in small open economies.

3

Studies using micro data (banks or corporations) include Bernanke, Gertler and Gilchrist (1996) and

Kashyap and Stein (2000).

4

Other such studies include Borio and McGuire (2004) and Pagan and Sossounov (2003). Terrones

(2004) studies the synchronization of house prices and the interaction between housing markets and

the real economy using dynamic factor models.

10

analyzed using a comprehensive dataset of a large number of countries over a long period of

time. Besides analysis that was limited in number of cases and some other, “case-type”

studies of individual episodes, or studies that focused specifically on the behavior of real and

financial variables surrounding financial crises, notably Reinhart and Rogoff (2008), to the

best of our knowledge, there is no comprehensive empirical analysis of these links.

5

Our paper thus fills three gaps in the literature. First, we examine the implications of

episodes of recessions, credit crunches, house and equity price busts for a large set of

macroeconomic and financial variables for a sizeable number of countries over a long period

of time. Second, our study is the first detailed, cross-country empirical analysis addressing

the implications of recessions when they coincide with certain types of financial market

difficulties, including credit crunches, house price busts and equity price busts. Third, we

provide some preliminary evidence suggesting that the change in house prices during

recessions appears to be an important factor influencing the cost of recessions.

The paper is structured as follows. In section II, we briefly present the data and methodology

we use. Next, we examine the basic characteristics of recessions in Section III. Then, we

consider how the key macroeconomic and financial variables behave around the episodes of

credit contractions (and crunches) and asset price declines (and busts) in Section IV. We

study the implications of recessions associated with crunches and asset price busts in

Section V. In Section VI, we briefly analyze the outcomes of recessions accompanied with

large increases in oil prices. This is followed by a short discussion of the changes in policy

variables during various episodes of recessions, crunches and busts in Section VII.

Section VIII presents a more formal analysis of the roles played by financial factors in

determining the cost of recessions using some simple regression models. Section IX

concludes.

II. DATABASE AND METHODOLOGY

A. Database

We construct a comprehensive database of macroeconomic and financial variables for 21

OECD countries over the period 1960:1-2007:4, mostly from the IMF International Financial

Statistics (IFS) and OECD Analytical Databases.

6

We focus our analysis on the following

macroeconomic variables: output, consumption, investment, residential investment, non-

residential investment, industrial production, exports, imports, net exports, current account

balance, and the unemployment and inflation rate. The quarterly time series of

5

Ferguson (2005) considered, in the aftermath of the collapse of the internet bubble, the links

between asset prices, credit and business cycles for three episodes with rapid asset price increases and

credit expansions, followed by subsequent recessions: the United Kingdom in 1974, Japan in 1992,

and the United States in 2001.

6

The countries in our sample are Australia, Austria, Belgium, Canada, Denmark, Finland, France,

Germany, Greece, Ireland, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Spain,

Switzerland, Sweden, the United Kingdom, and the United States.

11

macroeconomic variables are seasonally adjusted, whenever necessary, and in constant

prices.

The financial variables we consider are credit, house prices and equity prices. Credit series

are obtained from the IFS and defined as claims on the private sector by deposit money

banks. The main source for house prices is the Bank for International Settlements (BIS).

Equity price indices are also from the IFS. All financial variables are converted into real

terms by deflating them by the respective consumer price index (CPI).

The “policy” variables we focus on are government consumption, as a proxy for fiscal policy,

and short-term interest rates, as a proxy for monetary policy. The series for government

consumption are obtained from the OECD Analytical Database. The short-term interest rates

are from the IFS, Haver Analytics and Datastream. We consider the short-term interest rates

both in nominal and real terms, with the nominal rates deflated using the CPI to arrive at the

real rates. Government consumption is also deflated using the CPI. We list the detailed

sources and definitions of each of these variables in Appendix I.

B. Methodology

Much research has been devoted to the definition and measurement of business cycles

(Harding and Pagan, 2006). Our study is based on the “classical” definition of a business

cycle mainly because of its simplicity, but also because it constitutes the guiding principle of

the National Bureau of Economic Research (NBER) in determining the turning points of

U.S. business cycles. The definition itself goes back to the pioneering work of Burns and

Mitchell (1946) who laid the methodological foundation for the analysis of business cycles

in the United States.

In particular, they define a cycle to “consist[s] of expansions occurring at about the same

time in many economic activities, followed by similar general recessions, contractions, and

revivals which merge into the expansion phase of the next cycle; this sequence of changes is

recurrent but not periodic; in duration, business cycles vary from more than one year to ten

or twelve years.” Following the spirit of this broad characterization of a business cycle, the

NBER (2001) defines a recession as “a significant decline in activity spread across the

economy, lasting more than a few months, visible in industrial production, employment, real

income, and wholesale-retail trade. A recession begins just after the economy reaches a peak

of activity and ends as the economy reaches its trough.”

The classical methodology focuses on changes in the level of economic activity to identify

business cycles. As an alternative methodology, one can consider how economic activity

fluctuates around a trend by employing a method that extracts this trend in activity and then

identify a “growth cycle” as a deviation from this trend (Stock and Watson, 1999). The

classical methodology we employ, however, is particularly useful for our purpose since we

are interested in business cycles in OECD countries where growth rates have been relatively

low. This implies that growth recessions are small in size and can be frequent, while level

recessions are more pronounced, but fewer (Morsink, Helbling and Tokarick, 2002). The

classical methodology also allows us to focus on a well-defined set of cyclical turning points

12

rather than having to consider how the characterization of business cycles depends on the

specific detrending method used.

7

The turning points identified by our methodology are also

robust to the inclusion of newly available data, whereas new data can affect the estimated

trend and thus the identification of a growth cycle.

The methodology we use determines the peaks and troughs of any given series by first

searching for maxima and minima over a given period of time. It then selects pairs of

adjacent, locally absolute maxima and minima that meet certain censoring rules requiring a

certain minimal duration of cycles and phases. In particular, we employ the algorithm

introduced by Harding and Pagan (2002a), which extends the so called BB algorithm

developed by Bry and Boschan (1971), to identify the cyclical turning points in the log-level

of a series.

8

A complete cycle goes from one peak to the next peak with its two phases, the

contraction phase (from peak to trough) and the expansion phase (from trough to peak). The

algorithm requires that the minimum duration of the complete cycle and each phase must be

at least five and two quarters, respectively.

9

Specifically, a peak is reached in a quarterly

series y

t

at time t if:

-2 -1 2 1

{[( - ) 0, ( - ) 0] [( - ) 0, ( - ) 0]}

tt tt t t t t

yy yy and y y y y

++

>> < <

Similarly, a cyclical trough is reached at time t if:

-2 -1 2 1

{[( - ) < 0, ( - ) < 0] [( - ) > 0, ( - ) > 0]}

tt tt t t t t

yy yy and y y y y

++

We employ this algorithm to identify cycles in a variety of macroeconomic and financial

variables. Our main macroeconomic variable is output (GDP) which provides the broadest

measure of economic activity. Besides output, we also look at cycles in a number of

macroeconomic variables, including consumption and investment. In terms of financial

variables, we are interested in cycles in three variables: credit, house prices and equity prices.

The main characteristics of cyclical phases are their duration and amplitude (Harding and

Pagan, 2002a). Since we are mainly interested in examining contractions, we define these

7

There have been a large number of studies documenting that the features of growth cycles can

depend on the detrending method used (Canova, 1998).

8

The algorithm we employ is called the BBQ algorithm since it is applicable to quarterly data. It is

possible to employ a different algorithm, such as a Markov Switching (MS) model (Hamilton, 1989),

to date the turning points. Harding and Pagan (2002b) compare this method with their BBQ algorithm

and conclude that their algorithm is preferable because the MS model depends on the validity of the

underlying statistical framework (see also Hamilton (2003) on this issue). Also using this

methodology, Artis, Kontolemis, and Osborn (1997), Artis, Marcellino, Proietti (2002), Harding and

Pagan (2002a), Cotis and Coppel (2005), and Hall and McDermott (2007) analyze the main features

of business cycles, including cyclical phases and synchronization.

9

In the case of asset prices, the constraint that the contraction phase last at least two quarters is

ignored if the quarterly decline exceeds 20 percent. This is because asset prices can have much more

intra-quarter variation, making for large differences between peaks and troughs based on end-of-

quarter data and those based on higher frequency data.

13

characteristics for contractions only. The duration of a contraction, D

c

, is the number of

quarters, k, between a peak and the next trough. The amplitude of a contraction, A

c

, measures

the change in y

t

from a peak (y

0

) to the next trough (y

k

), i.e., A

c

= y

k

– y

0

. For output, we also

consider another widely used measure, the cumulative loss. This measure combines

information about the duration and amplitude of a phase to proxy the overall cost of a

cyclical contraction, likely of particular interest to policy makers. The cumulative loss, F

c

,

during a contraction, with duration k, is then defined as:

0

1

()

2

c

k

c

j

j

A

Fyy

=

=−−

∑

.

We further classify recessions based on the extent of decline in output. In particular, we call

recessions mild or severe if the peak-to-trough output drop falls into the bottom or top

quartile of all output drops during recessions, respectively. Likewise, declines in asset prices

and credit contractions are distinguished according to their severity. An equity (or house)

price bust is defined as a peak-to-trough decline which falls into the top quartile of all equity

(or house) price declines (Helbling and Terrones, 2003). Similarly, a credit crunch is defined

as a peak-to-trough contraction in credit which falls into the top quartile of all credit

contractions.

10

We identify 122 recessions in output (30 of which are severe), 112

contractions (28 crunches) in credit, 114 declines (28 busts) in house prices, 234 declines (58

busts) in equity prices.

In line with the way we date events in general, we next use a simple “dating” rule regarding

whether or not a specific recession is associated with a credit crunch or asset price bust. In

particular, if a recession episode starts at the same time or after the beginning of an ongoing

credit crunch or asset price bust, we consider the recession to be associated with the

respective credit crunch or asset price bust.

This rule, by definition, basically describes a

“timing” association (or coincidence) between the two events but does not imply a causal

link.

11

Among these events, there is a considerable overlap, since there are 18, 34 and 45 recession

episodes associated with credit crunches, house price busts and equity price busts,

respectively (Figure 1 provides the Venn diagram of the associations of recessions, crunches

and busts).

12

In other words, in about one out of six recessions, there is also a credit crunch

10

We rely on the changes in the volume of (real) credit to identify the episodes of credit crunches,

which is often defined as an excessive decline in the supply of credit that cannot be explained by

cyclical changes (see Bernanke and Lown, 1991). It is difficult to separate the roles played by

demand and supply factors in the determination of credit volume in the economy. An alternative

methodology to identify credit crunch episodes would be to consider an interest rate measure, i.e.,

track changes in the price of credit over time. We plan to explore this in future research.

11

An example of the fact that “association” does not describe causality is when exogenous shocks

cause a recession that otherwise would not have happened even when a credit crunch or asset price

bust was already occurring.

12

Although we have 34 recessions associated with housing busts, we have only 28 episodes of

housing busts. This is since housing busts last much longer than recessions do, and some housing

(continued…)

14

underway and in about one out of four recessions, also a house price bust. Equity price busts

overlap for about one-third of recession episodes.

13

Our algorithm closely replicates the dates of U.S. business cycles as determined by the

NBER Business Cycle Dating Committee. According to the NBER, the United States has

experienced 7 recessions over the 1960-2007 period and our algorithm provides exact

matches for 4 out of these 7 peak and trough dates and is only a quarter early in dating the

remaining peaks and troughs. The differences between our dates and the NBER ones stem

from the fact that the NBER uses monthly data for various activity indicators (including

industrial production, employment, personal income net of transfer payments, and the

volume of sales of the manufacturing and wholesale retail sectors), whereas we solely

employ quarterly series on output to identify the cyclical turning points. Nevertheless, the

main features of business cycles based on the turning points we document are quite similar to

those of the NBER. The average duration of U.S. business cycles based on our turning

points, for example, is the same as that reported by the NBER. In addition, the average

amplitude of cycles derived from our methodology is very close to that of the NBER cycles.

14

III. WHAT HAPPENS DURING RECESSIONS?

In this section, we first examine a set of basic stylized facts about recessions, including their

duration, amplitude, and cumulative output loss, and how these features vary across

countries. We then document the changes in our main macroeconomic and financial variables

during recessions. This is followed by an analysis of the temporal behavior of these same

variables around recessions. Last, we analyze the synchronization of recessions across

countries.

A. Basic Features of Recessions: Duration and Cost

Table 1A presents the main characteristics of recessions for each country in our sample.

Throughout the paper, we most often focus on medians because they are less affected by the

presence of outliers in our sample. Wherever relevant, however, we also refer to means. A

typical OECD country experienced about five recessions over the 1960-2007 period. There is

no apparent pattern across countries in the number of recessions, but some countries do stand

out. For example, Canada, Ireland, Japan, Norway and Sweden witnessed only three

recessions during this period, while Italy and Switzerland had 9 recessions, and New Zealand

busts are associated with multiple recessions. In particular, there are five housing busts that overlap

with two recessions each, and two busts that overlap with three recessions each.

13

Overlaps of recessions with credit contractions and asset price declines are numerous and we

briefly examine the implications of such overlaps in the later sections. The dates of the cyclical

turning points are available upon request.

14

In particular, the average peak-to-trough decline in output during the U.S. recessions is around

-1.7 percent based on our dates while it is -1.4 percent based on the NBER dates. We provide a

detailed discussion of the implications of recessions in the United States in Claessens, Kose and

Terrones (2008).

15

12, the most.

15

A typical recession lasts about 4 quarters (one year) with relatively small

variation across countries—the shortest recession is 2 quarters and the longest 13 quarters.

Roughly one-third of all recessions are short with only 2 quarters. The proportion of time

spent in recession, defined as the fraction of quarters the economy is in recession over the

full sample period, is typically around 10 percent.

16

In addition to duration, we describe the severity of a recession using two other metrics. The

median (average) decline in output from peak to trough, the recession’s amplitude, is about

1.9 (2.7) percent. It ranges from about 1 percent for the typical recession in Austria, Belgium,

Ireland and Spain to more than 6 percent for those in Greece and New Zealand. The

cumulative loss of a typical (median) recession is about 3 percent, but the average loss is

about 6.4 percent since the distribution is skewed to the right (there is on average a small

positive correlation (0.34) between duration and amplitude). This also shows that the overall

loss can differ quite a bit from amplitude as durations vary. Country examples further

illustrate this difference. For example, while the median amplitude of recessions in Finland

and Sweden are not as large as those in Greece and New Zealand, recessions in Finland and

Sweden have very large cumulative output losses (23 and 16 percent, respectively) since their

recessions are long.

As mentioned, a recession is classified as a severe one when the peak-to-trough decline in

output is in the top-quartile of all output declines during recessions, which means a peak-to-

trough output decline below -3.2 percent. While many OECD countries, including Austria,

Belgium, France, Ireland, Norway, Spain, and the United States, did not experience a severe

recession in the sample period, most recessions in Greece and New Zealand fell in this

category. The 30 such recessions we document are typically five quarters long, more than a

quarter longer than the average recession. They are, by construction, much more costly than

other recessions with a median decline of about 5 percent, almost three times that of other

recessions, and have a cumulative loss of about 10 percent, five times that of the other

recessions. An extremely severe recession, in which the peak-to-trough decline in output

exceeds 10 percent, is usually called a depression, of which there are 5 in our sample. The

last such depression episode took place in Finland in the early 1990s with an output decline

of 14 percent.

17

15

New Zealand has the highest number of recessions primarily because of the highly volatile nature

of its output fluctuations and its large exposure to terms-of-trade shocks. Consistent with this, the

number of recessions in other variables of New Zealand, including consumption, investment and

industrial production, also is quite high. The dates of New Zealand’s business cycles we report are

largely consistent with those reported in Morsink, Helbling, and Tokarick (2001) which documents

seven recessions over the 1973-2000 period. Hall and McDermott (2006), using unpublished output

data, identify 9 recessions for New Zealand during the 1946:1-2005:4 period.

16

The proportion of time a country spends in recession relates of course closely to the number of

recessions the country experienced (the correlation between the two is 0.9). The number and average

duration of recessions have, however, a small negative correlation (-0.26) since some countries

experienced many short recessions in relatively brief periods. For example, New Zealand had five

short recessions during the 1970s and Japan witnessed its three recessions after 1992.

17

The 5 depressions that occurred are: New Zealand (1966:4-1967:2); New Zealand (1974:3-1975:2);

New Zealand (1976:4-1978:1); Greece (1973:4-1974:3); and Finland (1990:1-1993:2). While the

(continued…)

16

As shown in Figure 2, most recessions lasted 4 quarters or less, and most of these were also

mild to moderate in depth, i.e., less than a 3.2 percent output decline.

18

Of the severe

recessions in our sample, only 40 percent were long, i.e., lasted more than 5 quarters. There

is also a pattern of recessions becoming shorter and milder over time, especially after the

mid-1980s. In particular, the amplitude of a typical recession fell from 2.6 percent in 1973-

1985 to 1.4 percent in 1986-2007. These patterns are in line with recent empirical work

documenting a trend decline in output volatility in industrial countries, the so called “Great

Moderation” phenomenon.

19

B. Changes in Macroeconomic and Financial Variables

We next examine how the main macroeconomic and financial variables typically vary during

a recession. Table 1B presents the peak-to-trough changes for these variables for all, severe,

and other recessions, which are those not in the group of severe ones. We find the expected

patterns in recessions in the sense that most macroeconomic variables exhibit procyclical

behavior. Not surprisingly, differences between severe and non-severe (other) recessions are

often statistically significant in terms of their durations, amplitudes and cumulative output

losses. In a severe recession, consumption typically drops by more than 1 percent, compared

to almost no change in other recessions. The importance of investment for explaining the

business cycle has been stressed in the literature for a long time. Indeed, both residential and

total investment tend to decline by double digits in severe recessions, compared to a drop of

about 4 percent in other recessions.

Recessions often also overlap with declines in international trade. Exports drop more in

severe recessions compared to other recessions (and significantly so). As expected, imports

fall, by six times more than exports in a typical recession and by close to 10 percent in severe

recessions (statistical significantly more so than in other recessions). While both net exports

and the current account balance register improvements during recessions, the changes are not

statistical significantly different across the types of recessions.

The fall in industrial production tracks closely the drop in investment in all types of

recessions and is larger than that of output. Recessions often coincide with an increase in the

unemployment rate (in 90 percent of cases). The unemployment rate typically rises three

times as much in severe recessions than in other recessions. Inflation typically drops slightly

(in 60 percent of all recessions), as expected given that aggregate demand is often down in

recessions, but inflation does not seem to vary between the types of recessions, possibly as

some severe recessions have been of the stagflation type⎯a recession combined with an

depression in Finland was the longest one with 13 quarters, the deepest one was the one in New

Zealand leading to roughly 15 percent reduction in output over the 1976:4-1978:1 period. See Kehoe

and Prescott (2002) for a discussion of a number of depressions in the 20

th

century.

18

To be more specific, around 35 percent of all recessions are short with 2 quarters, 40 percent are

medium duration of 3-4 quarters, and 25 percent are long with 5 quarters or more.

19

Explanations for this decrease are many, ranging from “the new economy” driven changes to the

use of effective monetary policy during the recent period (see Blanchard and Simon, 2001; and Stock

and Watson, 2003).

17

acceleration in the rate of inflation. We discuss the implications of such recessions later in

the paper.

Next, we examine the changes in our key financial variables during recessions. Although

credit typically continues to grow, it does so only at about 1 percent, with its growth rate

especially low in the initial stages of recessions. Credit growth does not vary much, however,

between severe and other recessions. Both house and equity prices typically contract in

recessions, with larger declines in house prices in severe than in other recessions.

20

Reflecting

the generally more volatile nature of equity prices, the decline in equity prices is more than

twice that of house prices as the median equity price decreases by 16 percent in severe

recessions, or some 12 percent more than in other recessions.

We also study the quarterly changes in the main macroeconomic variables during recessions

and compare them with those during non-recession (expansion) periods. This exercise can be

seen as another way of evaluating the cost of recessions relative to the average growth rate of

the economy during expansionary periods. The median quarterly decline in output during

recessions is around -0.5 percent whereas during expansionary periods it is close to

0.9 percent. This suggests that a typical recession leads to roughly 1.5 percent decline in

output per quarter compared with the periods of expansions the countries normally enjoy.

The average rate of contraction in consumption was much smaller than that in output with

0.03 percent per quarter, but the rate of growth during expansions was close to 0.75 percent.

More volatile variables of national income exhibit sharper differences in growth across the

periods of recessions and expansions.

C. Dynamics of Recessions

We next examine how various macroeconomic, trade and financial variables behave around

recessions (see Figure 3). We focus on patterns in the year-on-year growth in each variable

over a 6-year window—12 quarters before and 12 quarters after a peak.

21

All panels include

the median growth rate, i.e., the typical behavior, along with the top and bottom quartiles. As

noted, according to our definition, the bottom quartile includes the severe recessions, while

the top quartile contains the mild ones.

The evolution of output growth around a recession is as expected. Following the peak at date

0, output tends to register a negative annual growth rate after 3 quarters, and its growth rate

goes down to -1 percent at the end of the fourth quarter after the peak. In severe recessions,

the growth rate falls to -2 percent at that time. Although consumption does not decrease on a

year-to-year basis in a typical recession, it does fall during the first year of a severe recession.

In terms of timing, the evolution of consumption around recessions resembles the behavior of

output.

20

Credit declines during recessions in only around 35 percent of cases while house prices fall in

around 55 percent of all recessions and equity prices register a fall in about 60 percent of them.

21

In our figures, we focus on year-on-year changes in the relevant variables since quarter-to-quarter

changes are often quite volatile and provide a noisy presentation of recession dynamics.

18

Some macroeconomic variables naturally show early signs of a slowdown before the

recession starts. For example, residential investment typically declines sharply ahead of the

onset of recessions. Moreover, both components of investment (residential and non-

residential) often register negative year-to-year changes already in the first quarter of a

recession, i.e., three quarters ahead of output, and their growth rates typically stay negative

for up to 6 quarters implying that the recovery in investment often starts later than that in

output. In severe recessions, recovery of the growth rate of investment can take up to three

years.

Industrial production also shows signs of weakness early on and typically registers a sharp

decline before a recession starts. During the onset of recessions, inflation is typically still on

an increasing path, and unemployment is already starting to rise. After the recession starts,

however, the rate of inflation declines while the increase in the unemployment rate

accelerates. Unemployment is a good leading indicator of economic activity as it typically

begins climbing a quarter ahead of recessions but stays compressed more than a year after the

end of the recession.

In terms of trade variables, the growth rates of both exports and imports slow down in a

recession, but that of imports much more. The growth rate of imports often tends to fall

before the recession starts and can decline to -7 percent in the first year of a severe recession.

While both net exports and the current account balance improve during a typical recession,

the improvement in net exports is often earlier and more pronounced than that of the current

account.

Credit growth also slows down, by some 2 to 3 percentage points before a recession starts,

and then by another 2 percentage points over the recession period, typically not returning to

pre-recession growth rates for at least three years after the recession started. Recessions are

often also proceeded by slowdowns in the growth rates of asset prices. In the first year of a

typical recession, for example, house and equity prices decline on a year-to-year basis by

roughly 3 and 16 percent, respectively. While equity prices often start registering positive

growth after about six quarters, house prices typically decline during the two years after the

end of a recession.

D. Synchronization of Recessions, Credit Contractions and Asset Price Declines

We next examine the synchronization of recessions, credit contractions and asset price

declines across countries. Our synchronization measure is simply the fraction of countries

experiencing the same event at the same time.

22

For recessions, Figure 4 shows how this

fraction evolves over time along with the dates of recessions in the United States. The figure

shows recessions bunching in about four periods during 1960–2007. First, a large fraction of

22

Recent research has typically relied on three main measures of synchronization. The first is bilateral

output correlations, which capture co-movements in output fluctuations of two countries. The second

is the share of output variances that can be attributed to synthetic (unobservable) common factors, as

in Kose, Otrok and Prasad (2003). The third one is the concordance statistic (Harding and Pagan,

2002a), which measures the synchronization of turning points.

19

countries went into recession in the mid-1970s, shortly after the first oil price shock. The

fraction of countries in recession also rose during the second oil price shock and the period of

highly synchronized contractionary monetary policies across major industrial economies in

the early 1980s. In the early 1990s, recessions were again highly synchronized around the

world, and in the early 2000s to some degree. In the first three of these four periods, more

than 50 percent of countries in our sample were in a recession at the same time. The peak

episodes of highly synchronized recessions quickly followed each other in some instances, as

shocks spilled from one country to the other. This was, for example, the case in the early

1990s because of the asymmetric shocks hitting countries across major currency areas (see

Morsink, Helbling and Tokarick, 2002).

23

We document in the same way the synchronization of turning points in consumption and

investment. A well known stylized fact of business cycles is that investment is much more

volatile than output and consumption is somewhat less volatile than output (Backus, Kehoe

and Kydland, 1995).

24

In our sample, indeed, investment declines in three-fourth of all

recessions while consumption contracts in only half of all recessions. Consistent with these

observations, the fraction of countries experiencing a period of investment (consumption)

contraction at any time is much higher (lower) than that of those experiencing recessions.

And, while investment contractions are highly synchronized, consumption contractions are

much less so. These results are consistent with recent findings suggesting that common

factors play a much larger role in explaining fluctuations in investment than they do in

consumption (Kose, Otrok and Prasad, 2008).

25

Recessions tend to coincide with contractions in domestic credit and declines in asset prices,

as documented in Section IIIC. This also shows up in the fraction of countries experiencing

recessions around the world being highly correlated with the fractions of those going through

credit contractions or bear asset markets (Figure 5). In particular, credit contractions are

closely associated with recessions. House price declines are also highly synchronized across

countries,

despite the fact that housing is a nontradable asset, and the degree of

synchronization rises especially during recession episodes.

26

Equity prices exhibit the highest

degree of synchronization reflecting the extensive integration of financial markets. However,

23

Kose, Otrok and Whiteman (2008) examine the degree of synchronization of G-7 business cycles

using a dynamic factor model. They report that a common factor, on average, explains a larger share

of the business cycle variation in G-7 countries since the mid-1980s compared to 1960–1972.

24

For a detailed analysis of the volatility and comovement properties of business cycles for a large set

of countries, see Kose, Prasad and Terrones (2003a, 2003b).

25

We also analyze the synchronization of turning points in industrial production, exports and imports.

As expected, the proportion of countries experiencing a contraction in industrial production is very

closely correlated with that going through a recessionary period. The results indicate that

synchronized recessions across countries have particularly adverse effects on global trade flows as

evidenced by the higher fraction of countries experiencing contractions in their exports and imports

than those witnessing recessions. We also examine the fraction of countries experiencing both real

and financial cycles at the same time, such as recessions, credit contractions and/or asset price

declines. The results of these additional exercises are consistent with the findings we report here.

26

Terrones (2004) shows that house prices tend to move together across countries and they are

procyclical, rising in economic expansions and falling in recessions.

20

the popular saying that “Wall Street has predicted nine of the last five recessions” resonates

here as the fraction of countries experiencing bear equity markets frequently exceeds the

fraction of countries in a recession.

IV. WHAT HAPPENS DURING CREDIT CONTRACTIONS AND ASSET PRICE DECLINES?

In this section, we study the main features of the episodes of credit contractions and declines

in the prices of housing and equity in our sample. As we explained in Section II, credit

contractions and asset price declines that fall into the top quartile of all credit contractions

and asset price declines are classified as credit crunches and asset price busts, respectively. In

particular, when the peak-to-trough decline in credit exceeds 9.5 percent, it is called a crunch

episode, and when the decline in house (equity) price is larger than 14.3 (38.7) percent, it

qualifies as a house (equity) price bust. In the following sub-sections, we first document the

basic stylized facts of each of these credit contraction/crunch and asset price decline/bust

events and then examine the temporal patterns of various macroeconomic and financial

variables around these episodes.

A. Episodes of Credit Contractions

Table 2A shows the main features of credit contractions and crunches for each country in our

sample. There are 112 (28) credit contraction (crunch) episodes. A typical OECD country

went through about 6 credit contractions, but there is much variation across countries.

Germany, the Netherlands, and Spain witnessed only a few contractions (2 to 3) while

Greece, New Zealand and Portugal had the highest number (8). Austria, France, Germany

and Switzerland never experienced a credit crunch episode during the 1960-2007 period, but

the other countries in our sample had at least one.

The median (average) credit contraction episode lasts 4 (6) quarters. Credit crunches last

typically twice as long, 8 quarters, and are statistically significantly longer than non-crunch

(other) contraction episodes (Table 2B). Credit contractions usually mean some 4 percent

decline in credit from peak to trough. In case of crunches, the decline in credit is 17 percent,

significantly more than during the non-crunch episodes.

While output growth slows down, especially early on in a credit contraction or crunch

episode (as we show next), output typically is higher at the end than at the beginning of these

episodes. The increase in output during contractions and crunches is not surprising since

these episodes do not always fully overlap with recessions and last twice as long as

recessions do. Output also expands significantly more during crunches than during other

contractions, probably because the duration of a typical crunch episode is 5 quarters longer

than the duration of a typical non-crunch episode. Still, the average growth rate of output in

credit crunch episodes is less than half of that observed during other periods.

27

27

In particular, the quarterly growth rate of output is typically around 0.3 percent when there is a

credit crunch whereas it is more than 0.8 percent during other contraction episodes.

21

Credit contractions are associated with visibly strong negative effects on investment. In

particular, credit contractions (crunches) are typically accompanied with declines in

residential investment of about 1 (6) percent over the period when credit contracts. The

unemployment rate is typically flat during a credit contraction, but increases significantly

during a credit crunch episode, primarily because of job losses early on in these episodes

when economic activity also weakens.

With respect to other financial variables, house prices typically decline significantly more

during credit crunches, by some 10 percent versus 1 percent in the typical non-crunch

episode. While equity prices usually also decline somewhat during credit contractions, they

actually increase over the credit crunch episodes, perhaps anticipating a recovery from the

deeper credit slump and the longer duration of these episodes.

We then examine how the various macroeconomic and financial variables behave around

credit crunches (Figure 6). As for recessions, we focus on patterns in the year-on-year growth

in each variable over a 6-year window—12 quarters before and 12 quarters after a peak of

credit expansion. All panels include the median growth rates, i.e., the typical behavior, along

with the top and bottom quartiles. As before, the bottom quartile denotes the worst 25 percent

of all credit crunches and the top quartile the best 25 percent.

Output growth typically starts declining two quarters before the beginning of a credit crunch

and goes down by 2 percentage points after the fifth quarter. Although output growth

typically does not become negative on a year-to-year basis in a credit crunch, it does so in at

least one-quarter of the crunch episodes as evidenced by the bottom quartile. In a typical

credit crunch, the year-on-year growth rate in consumption goes down as well and can fall to

-2 percent in about five quarters in some crunch episodes.

As expected, investment weakens before the credit crunch starts. In particular, residential

investment typically starts to slow down much before the crunch episode begins, and actually

shrinks one quarter ahead of the start of the episode. Growth rates of total investment and

residential investment typically stay negative for up to 8 quarters. Moreover, investment can

take up to three years and residential investment even longer to recover in some episodes of

credit crunches, much longer than the duration of slowdown in output. Inflation is on an

increasing path and unemployment is already starting to rise prior to the start of a credit

crunch, but as activity slows down after the beginning of a crunch, the rate of inflation

declines and the increase in the rate of unemployment accelerates.

Credit crunches are generally preceded by a period of rapid expansion in credit, but are most

often accompanied by slowdowns in asset prices. The median (year-to-year) credit growth is

5 to 6 percent just before the peak of credit expansion is reached and then slows down

sharply over the crunch period, by more than 10 percentage points, falling to -6 percent and

not returning to positive levels until 10 quarters after the credit crunch started. The rapid

decline in credit during this period likely reflects both lower demand, e.g., decrease in

investment, but also a fall in supply due to bank capital shortfalls and other adverse supply

side effects. The figure shows the clear spillover effects from tight credit markets to the

housing and equity markets. In particular, house prices typically fall in the first year of a

22

credit crunch and continue to decline for at least three years after the beginning of a crunch

episode. Equity prices often decline before a credit crunch episode starts and further weaken

during the first year, but then frequently stage a recovery ahead of the pick up in credit.

B. Episodes of Declines in House Prices

Table 3A shows the main features of house price declines and busts for each country in our

sample. There are 114 (28) episodes of house price decline (bust) implying that a typical

country experienced around 6 such episodes. Australia and Canada had the largest number

(9) of decline episodes while Greece had only 1. While the majority of countries had at least

one house price bust over the 1960-2007 period, Australia, Belgium, Germany, Greece,

Portugal, the United Kingdom, and the United States did not experience any.

28

The typical

episode of a decline in house prices lasts 6 quarters, but housing busts usually last more than

16 quarters. While the typical (median) decline in house prices is only 6 percent, due to some

very large declines in the sample, the average decline is around 11 percent. During a house

price bust, prices decline by about 29 percent typically.

Like credit contractions, output typically still expands during episodes of house price

declines (Table 3B). As in the case of credit contractions, this mainly reflects that house price

declines last a long time during which output still grows, albeit at a much lower rate.

29

There

appears to be, however, a substantially adverse impact of house price declines on investment

(and its components) which is much larger than that in credit contractions. During periods of

house price declines (busts), residential investment typically shrinks by 4 (12) percent. Total

investment also goes down, typically, by more than 8 percent. While the unemployment rate

usually records a statistically significant increase during bust episodes relative to non-bust

(other decline) episodes, inflation tends to be much lower at the end of house price busts, by

some 3 percentage points. Credit still expands over the episodes of house price declines, but

at a slower rate than normal, and equity prices do not change much. These findings suggest

that developments in the housing market can have particularly strong links with the overall

economy.

Figure 7 presents the dynamics of the key macroeconomic and financial variables around the

periods of house price busts. Although the typical slowdown in output around a house price

bust is more gradual than that in a credit crunch, the dynamics of house price busts are

otherwise quite similar to those of credit crunches. The slowdown in output starts at the time

of the house price bust and is associated with a slowdown in consumption growth.

Investment declines largely occur after the onset of the house price decline and involve

contractions in both residential and nonresidential investment. While residential investment

declines less sharply after the first year of the beginning of a house price bust than that of a

credit crunch, the recovery of residential investment takes much longer in house price busts.

28

Since our study focuses on the completed events only, current declines in house prices in the United

States and some other advanced countries are not included in these calculations.

29

For example, the quarterly growth rate of output during house price busts is typically about one-

fourth of that in periods without busts.

23

After a few quarters, and often following a run-up, inflation typically experiences a sharp

decline, and unemployment starts to rise after about two years as the impact of the house

price decline is gradually felt more broadly. As noted, house prices remain on the decline for

long periods during a bust episode, typically much more than three years. While equity prices

start falling before the onset, they usually begin to recover within two years of a house price

bust. Credit growth experiences a large slowdown and does not return to the pre-bust levels

for at least three years.

C. Episodes of Declines in Equity Prices

Table 4A presents the main features of equity price declines and busts for each country in our

sample. Since equity prices are much more volatile than house prices, there are many more

episodes, 234 (58), of declines (busts) in equity than in house prices. In a typical country,

there were around 11 (3) episodes of equity declines (busts). While Italy had 7 equity bust

episodes, Greece, Spain and the United States experienced only one. Episodes of declines

vary quite a bit in terms of their durations and amplitudes across countries, but they typically

last 5 quarters and are associated with a price drop of 27 percent. Equity busts, however,

typically last 10 quarters and are accompanied with a 50 percent price decline.

As in the cases of credit contractions and house price declines, while both output and

consumption also continue to grow during episodes of equity price declines, they do so at

lower rates than typical (Table 4B).

30

However, different than for credit contractions and

house price declines, there is no decline in investment over the episodes of equity price

declines. While unemployment picks up a little bit, the rate of inflation does not change

much during periods of equity price declines. Credit still registers an expansion and house

prices typically increase between the peak and trough of the equity price decline episodes. In

sum, equity price declines appear somewhat less related to the real economy than credit

contractions or house prices declines.

The weak connection between the dynamics of equity prices and economic activity is also

reflected in the behavior of the main macroeconomic variables (Figure 8). The growth rate of

output slows down, but this usually starts only three quarters after the beginning of the equity

bust and is much more limited, with the level of output typically not experiencing a decline.

The extent of slowdown in consumption growth associated with an equity price bust is also

delayed—until after one year or so, and is weaker than that observed during credit crunches

and house price busts. The decline in investment growth follows with a relatively long lag the

start of the equity price bust—only after 3 to 4 quarters does investment growth slow down.

The growth rate of non-residential investment increases for a few quarters after the start of

the bust, before falling at a much faster rate than residential investment growth. Inflation

30

The median quarterly growth rate of output during equity busts is typically around 0.5 percent

while it is about 0.8 percent during the periods without such busts. Other variables, including

consumption, investment and its components, also register weaker growth during the episodes of

equity busts relative to other periods.

24

typically remains elevated and unemployment experiences only a very small increase after an

equity price bust.

The fall in equity prices itself is a sharp and prolonged one as prices do not start to recover