OFFICE OF THE STATE ASSESSOR

DEPARTMENT OF COMMERCE, COMMUNITY

AND ECONOMIC DEVELOPMENT

Property Taxation 101 – The Basics

Or…..

How does this thing really work?

January 25, 2016

PropertyTax101

PartI–CalculatingYourPropertyTaxBillPg.4

PartII– DeterminingtheTaxRatePg.11

PartIII–WhatAboutExemptions?Pg.31

PartIV– CappingtheMillageRatePg.47

StateAssessor

2

Thefollowingpresentationandcontentare

intendedtoillustratethefundamental

basicsofthepropertytaxsystem.Assuch,

thisisa“barebones”exampleprovidedto

illustratefundamentalmathematicsofthe

propertytaxes.Inpractice,property

taxationandbudgetingaremorecomplex

andincludemanymorecomplextopicsthat

are

notcoveredordiscussedhere.

StateAssessor

3

PARTI

CALCULATING

YOUR

PROPERTYTAXBILL!!

StateAssessor

4

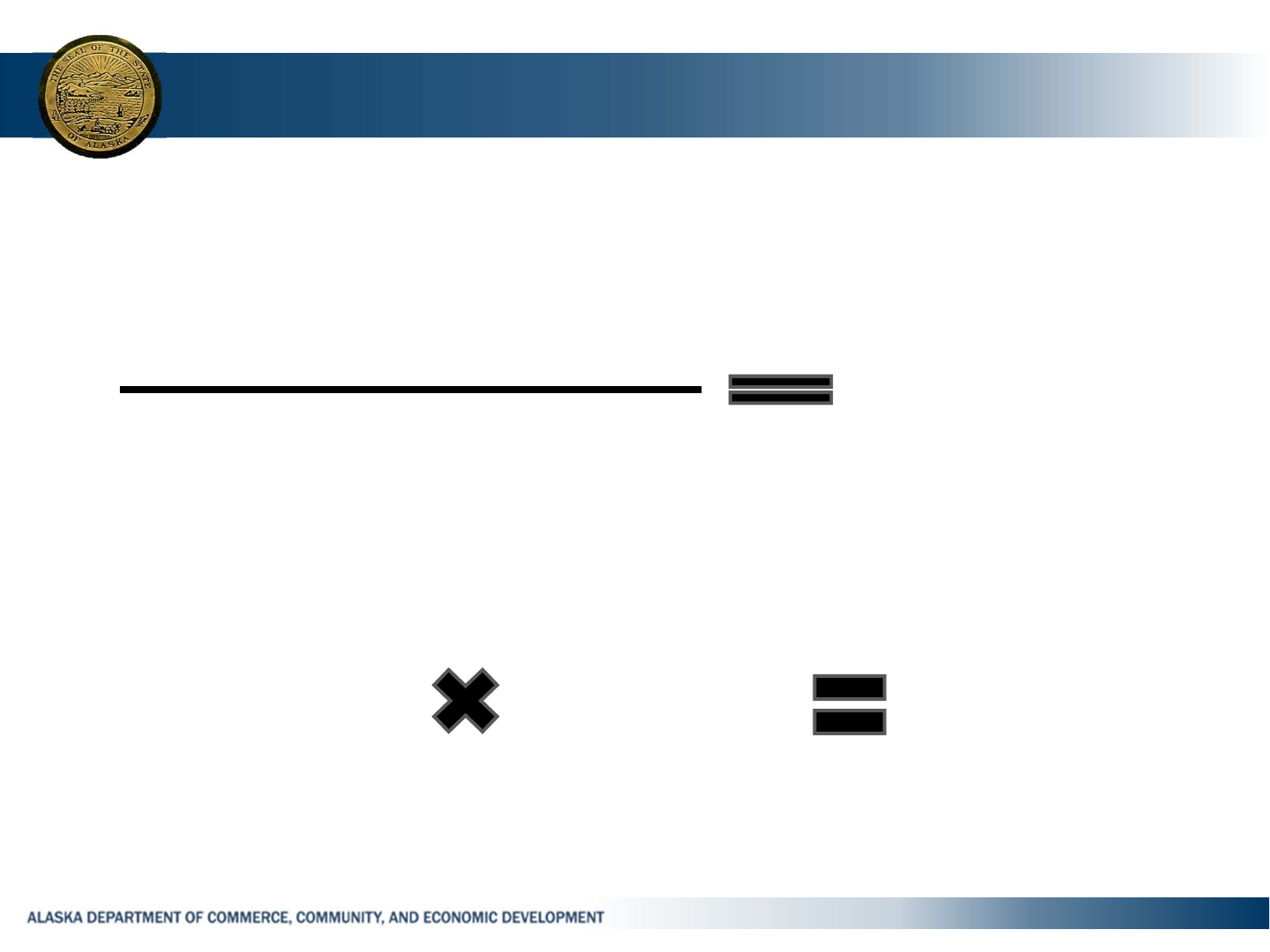

PropertyTaxesarebaseduponarelatively

simpleequation.

AssessedValueXMillageRate=TaxBill

Theonlyinformationneededtocalculateyour

propertytaxbillaresomedefinitionsforthree

terms;AppraisedValue,AssessedValueand

MillageRate.

StateAssessor

5

AppraisedValue

Thisisthemarketvalueofyourpropertyas

determinedbythelocalassessor.Theappraised

valueofyourpropertyvariesasthemarketfor

realestatefluctuates.Ifmarketvaluesdecrease,

appraisedvalueswilldecreaseandifmarket

valuesincreaseyourappraisedvaluewill

increase.Ultimately,theappraisedvalueofyour

propertyisafunctionoftransactionsofreal

estateinthelocalmarket.

StateAssessor

6

AssessedValue

Thisisthetaxablevalueofyourproperty.

Thiswilloftendifferfromtheappraisedor

“marketvalue”ofapropertydueto

exemptions.Forexample,theappraised

valueofapropertymaybe$200,000,butif

thepropertyis10%exempt,theassessed

valuewouldonlybe$180,000.Propertytax es

arecalculatedontheassessedvalue,notthe

appraisedvalue.

StateAssessor

7

MillageRate

Thetaxratethatisappliedtotheassessed

value.Themillagerateor“millrate”isusually

anexpressionofdollarsoftaxleviedperevery

$1,000ofvalue.Soamillagerateof12.5

wouldmeanthatforevery$1,000ofassessed

value,thetaxpa yerwouldpay$12.50in

tax.A

millrateof12.5canalsobeex pressedas

1.25%or0.0125indecimalform.

StateAssessor

8

CalculatingtheTaxBill

Sowhatwouldthetaxbillbefora

propertywithanappraised valueof

$200,000,anexemptionof10%anda

millagerateof12.5?

StateAssessor

9

TheTaxBill

AppraisedValue:$200,000

‐ 10%Exemption:‐$20,000

AssessedValue:$180,000

XMillageRate0.0125

=PropertyTaxBill$2,250

StateAssessor

10

PARTII

DETERMINING

THE

TAXRATE!

StateAssessor

11

TheTaxRateisdeterminedduringthebudget

processofthelocaltaxingauthority.In

Alaska,thiswillbeyourboroughandorcity.

Eachyearyourcommunitywillsetabudget

thatdetailstheexpenditurestheywillmake

andthesourcesofrevenuethatwillbe

collectedandusedto

fundthatbudget.A

currentexampleoftherevenuesourcesfora

majorAlaskacommunityfollows.

StateAssessor

12

StateAssessor

13

STATE &

FEDERAL 25%

PROPERTY TAX

15%

SALES TAX

14%

OTHER TAXES

2%

CHARGES FOR

SERVICES

37%

OTHER & MISC

7%

REVENUESBYSOURCE

Thesourcesofrevenuevaryfrom

communitytocommunityforvarious

reasons.Forexample,somecommunities

haveasalestaxandsomedonot.Others

mayhaveoilandgaspropertiesandsome

donot.Somemayreceivefishtax esor

obtainsubstantialrevenuefromtourism

relatedbusinesses.However,forthis

presentationwewillusetherevenue“mix”

providedhere,withpropertytaxessetat

15%oftherevenuescollected.

StateAssessor

14

Now,justforpurposesofexample,let’s

createanewcommunityandtheirbudget.

Let’scallit……

ALASKAVILLE!

StateAssessor

15

State & Federal

$2,500,000

25%

Property Tax

$1,500,000

15%

Sales Tax

$1,400,000

14%

Other Taxes

$200,000

2%

Charges for

Services $3,700,000

37%

Other & Misc.

$700,000

7%

ALASKAVILLEREVENUESBY

SOURCE

StateAssessor

16

Alaskaville hasjustcompletedit’s

budget.Totalexpendituresinthebudget

aresetat$10,000,000forthefiscalyear.

Ofthisamount,cityofficialsestimate

thattheywillreceive$8,500,000in

revenues fromvarioussourcesand

$1,500,000or15%ofthetotalbudget

willcomefromlocalpropertytax es.

StateAssessor

17

Notethatthisisafairlytypicalanalysis.Local

officialshavelimitedcontrolovermanysources

ofrevenuesuchassalestaxorfederalandstate

money.Theamountoflocalsalestaxdepends

onconsumerpurchases.Federal&statefunding

isdecidedbyfederalandstateofficials.While

thesesources

canbeestimated,theycannotbe

fixed.Onlytheamountofthepropertytaxis

trulyunderlocalcontrol.So,thepropertytaxis

oftenusedasthefinalbuildingblocktoclose

andbalancethebudget.

StateAssessor

18

What’stheMillageRate?

Asnotedearlier,Alaskaville hassetits

budgetat$10,000,000.Tofundand

balancethisbudget,theyhave

dedicated$1,500,000inproperty

tax es.Thisiscommonlyreferredtoas

thePropertyTaxLevy.

StateAssessor

19

So,thequestionis….

Whattaxratemust

Alaskaville settocollect

$1,500,000inproperty

taxes?

StateAssessor

20

StateAssessor

21

To answer this question one must

know the basic formula for

calculating property tax rates.

Property Tax Levy

Property Tax Base

Millage

Rate

StateAssessor

22

We’ve already discussed the Property Tax

Levy, but what is the Property Tax Base?

Property Tax Base: The sum of all

Assessed Values in the jurisdiction.

And we must remember, that Assessed

Values are used, not the Appraised Values

which can be substantially different.

StateAssessor

23

And now let’s return to Alaskaville.

The Assessor tells us that assessed values

of the tax roll for Alaskaville add up to

$120,000,000 for the tax year. This is the

Property Tax Base for the current tax year.

So what is the required millage or “mill”

rate for Alaskaville?

StateAssessor

24

Let’s fill in the blanks in the formula!

Property Tax Levy

Property Tax Base

Millage

Rate

$1,500,000 (Levy)

$120,000,000 (Base)

0.0125

Mill Rate

So we know Alaskaville needs a millage rate

of 0.0125, which could also be stated as

1.25% or $12.50 per $1,000 of assessed

value.

StateAssessor

25

Scenarios

Given these basics of how property

taxes work, we can also portray different

scenarios of what the tax rate and taxes

would be given different situations for

Alaskaville.

StateAssessor

26

Scenario: Original levy and tax base, no changes.

$1,500,000 (Levy)

$120,000,000 (Base)

0.0125

Mill Rate

Taxes on a property assessed at $100,000:

$100,000 0.01250 $1,250

StateAssessor

27

Scenario: Tax Base (Values) increased by 5%

$1,500,000 (Levy)

$126,000,000 (Base)

0.0119

Mill Rate

Taxes on a property assessed at $100,000: As values have

increased by 5%, the property has also increased to $105,000.

$105,000 0.0119 $1,250

StateAssessor

28

Scenario: Tax Base (Values) decreased by 5%

$1,500,000 (Levy)

$114,000,000 (Base)

0.0132

Mill Rate

Taxes on a property assessed at $100,000: As values have

decreased by 5%, the property has also decreased to $95,000.

$95,000 0.0132 $1,254

StateAssessor

29

Scenario: Property Tax Levy increased by 5%

$1,575,000 (Levy)

$120,000,000 (Base)

0.0131

Mill Rate

Taxes on a property assessed at $100,000:

$100,000 0.0131 $1,310

StateAssessor

30

Scenario: Property Tax Levy decreased by 5%

$1,425,000 (Levy)

$120,000,000 (Base)

0.0119

Mill Rate

Taxes on a property assessed at $100,000:

$100,000 0.0119 $1,190

PARTIII

WHAT

ABOUT

EXEMPTIONS?

StateAssessor

31

StateAssessor

32

How do exemptions work?

What overall effects do property tax

exemptions have on property taxes?

Let’s take a look at a very simple

example that more or less applies to

everyday life.

StateAssessor

33

It’s John’s Birthday! You and 8 other

friends (ten people total) decide to

take him out for a steak dinner to

celebrate. That was as many

people as we could get to attend

since John is the property tax

assessor and not to popular.

StateAssessor

34

The steakhouse down the street

says that for $500 they will serve us

all. So…

$500 10 people $50

Simple enough!

StateAssessor

35

But as we said, its John’s Birthday!

So we are all going to “chip in” and

pay for John’s meal.

We are going to exempt

John from paying.

So what is the “math” now?

StateAssessor

36

Originally the math was….

$500 10 people $50

But here is the math now….

$500 9 people $55.56

So that John can be exempted from

paying, we must each pay $5.56 more

for the math to work.

StateAssessor

37

Now let’s go back to Alaskaville and

see how it works with property

taxes.

Remember our original calculations

for the Alaskaville budget and

property tax rate?

StateAssessor

38

Scenario: Original

$1,500,000 (Levy)

$120,000,000 (Base)

0.0125

Mill Rate

Taxes on a property assessed at $100,000:

$100,000 0.0125 $1,250

StateAssessor

39

Now, what if we decided to assess all

residential property at 50% of value and

keep commercial property valued at

100%.

This is not allowed in Alaska, however

similar property tax policies do exist in

the Lower 48. Such policies are called

“Fractional Assessments”.

StateAssessor

40

John, remember he’s the assessor, tells

us that residential property is 75% of the

tax roll. So, in the original Tax Base…

Residential would be...

$120,000,000 75% $90,000,000

And Commercial would be…

$120,000,000 25% $30,000,000

StateAssessor

41

But if we exempt 50% of the value of

residential property our tax base would

look like this.

Residential would be:

$90,000,000 50% $45,000,000

Commercial would still be: $30,000,000

And the “new” Tax Base would be the

sum of the two or….. $75,000,000

StateAssessor

42

Scenario: 50% Exempt on Residential

$1,500,0000 (Levy)

$75,000,000 (Base)

0.0200

Mill Rate

The required millage rate has

increased dramatically due to the

change in the Property Tax Base. But,

what’s happened to the actual tax bills?

StateAssessor

43

Taxes on a residential property previously assessed at

$100,000: Now valued at $50,000!

$50,000

0.0200 $1,000

Taxes on a commercial property which would still be

assessed at $100,000:

$100,000

0.0200 $2,000

And remember that prior to the exemption, both properties

would have paid the same property tax of:

$1,250

StateAssessor

44

And what has happened to the total Property Tax Levy?

$45,000,000

0.0200

$900,000

Taxes on Commercial properties:

$30,000,000

0.0200

$300,000

So the total Property Tax Levy would be:

Taxes on Residential properties:

$1,500,000

Which is exactly what the Property Tax

Levy was prior to the exemption.

StateAssessor

45

Now, let’s summarize our results!

• The original millage rate of $12.5 per $1,000 of assessed

value increased to $20.00 per $1,000 of assessed value.

The residential exemption shrank the tax base such that a

60 percent increase was required in the millage rate.

• Residential properties were assessed at 50 percent less,

but due to the much higher millage rate their taxes

decreased by only 20 percent.

• Commercial properties were assessed just as before, so

the tax bill for these properties increased by 60 percent.

StateAssessor

46

And here’s a quick summary of the numbers for

Alaskaville showing the results before and after

implementing such an policy.

50%RESIDENTIAL

EXEMPTIONDATA

VALUE

BEFORE

VALU E

AFTER

VALU E

CHANGE

TAX

BEFORE

TAX

AFT ER

TAX

CHANGE

PROPERTYTAXLEVY $1,500,000 $1,500,000 0.0% N/A N/A N/A

PROPERTYTAXBASE $120,000,000 $75,000,000 ‐37.5% N/A N/A N/A

MILLRATE 0.0125 0.0200 60.0% N/A N/A N/A

$100KRESIDENTIAL $100,000 $50,000 ‐50.0% $1,250 $1,000 ‐20.0%

$100KCOMMERCIAL $100,000 $100,000 0.0% $1,250 $2,000 60.0%

PARTIV

CAPPING

THE

MILLAGERATE

StateAssessor

47

StateAssessor

48

Various efforts to modify the basic premise of Property

Taxation have been attempted over the years. One

approach has been to set a fixed or capped millage rate.

So what are the impacts to capping the millage rate?

To analyze this, we must return to the basic equation for

calculating the millage rate.

Property Tax Levy

Property Tax Base

Millage

Rate

StateAssessor

49

As we applied this formula previously, the property tax

base is fixed by the sales prices of real estate in the

market and the property tax levy was also fixed via the

budget process. Capping the millage rate converts this

element of the formula to a fixed value as well.

However, the basic math of the formula will not allow all

three variables to remain fixed over time. Or stated

another way, if the millage rate is fixed, any change in

the property tax levy or the property tax base will nullify

the validity of the equation.

A little bit of simple math with our Alaskaville case will

help to illustrate the situation.

StateAssessor

50

Our original millage rate calculation for Alaskaville was….

$1,500,000 (Levy)

$120,000,000 (Base)

0.0125

Mill Rate

And the equation as applied above holds true. That is to

say that the equation balances. Now let’s presume that

Alaskaville fixes the millage rate at 0.0125 from this year

into the future.

StateAssessor

51

In the subsequent year, the assessor reports that due to

market activity and new construction the property tax base

has increased by five percent to $126,000,000.

$1,500,000 (Levy)

$126,000,000 (Base)

0.0125

Mill Rate

The equation is now in a state of imbalance since the

millage rate of 0.0125 when applied to the new tax base

produces a property tax levy of $1,575,000. Yet,

Alaskaville only required a property tax levy of $1,500,000.

The city is taxing more than is required and has a surplus in

what had been a balanced budget.

StateAssessor

52

But what if the assessor had reported that the property tax

base had decreased by five percent to $114,000,000.

$1,500,000 (Levy)

$114,000,000 (Base)

0.0125

Mill Rate

The equation is again in a state of imbalance since the

millage rate of 0.0125 when applied to the tax base

produces a property tax levy of $1,425,000. Yet,

Alaskaville still requires a property tax levy of $1,500,000 to

fund the city. The city now has a budget deficit rather than

the previous balanced budget.

StateAssessor

53

Looking at the results we can see that the Property Tax Levy,

which was previously a fixed element of the formula, has

now, by mathematical necessity, become a “floating” number.

As well, the very configuration of the formula itself has

fundamentally changed.

PropertyTaxLevy

(FixedbyBudget)

PropertyTaxBase

(FixedbyMarket)

UncappedRate

Formula:

MillageRate

(Floating)

CappedRate

Formula:

MillageRate

(FixedbyMandate)

PropertyTaxBase

(FixedbyMarket)

PropertyTaxLevy

(Floating)

StateAssessor

54

Also note, that since the millage rate is now fixed,

the amount of the property tax levy will only vary

when there is a change in the property tax base.

Clearly this change presents some very significant

issues for the efforts of Alaskaville to produce a

truly balanced budget. Since the property tax levy

is now a “moving target”, Alaskaville will have a

more difficult time in estimating revenues. Thus,

their budget will tend to produce surpluses or

deficits depending upon the accuracy of the

estimates that are used in the budgeting process.

StateAssessor

55

Future surpluses to the property tax levy might be

addressed by providing that the millage rate cap

be a maximum level. This would allow Alaskaville

to use a rate less than the capped rate when a

surplus to the property tax levy might result.

However, what happens with a

DEFICIT?

StateAssessor

56

When the tax base decreased by 5 percent, we noted that

Alaskaville had a deficit of $75,000 in their budget. So

what can Alaskaville do to rectify this shortfall?

Alaskaville could re-open its budget and eliminate $75,000

of services that they had previously indicated they would

fund.

And/or…

Alaskaville could re-visit other sources of local revenue

such as sales taxes or fees and increase collections from

those sources to recover the “missing” $75,000 of revenue.

StateAssessor

57

In the end, capping the millage rate has increased the

difficulty of Alaskaville to produce a dependable, balanced

budget since revenue to fund the budget is now less

certain.

Budget surpluses and deficits will result as future changes

to the tax base arise due to new construction and the value

of real estate in the market. As well, it must be

remembered that the budgetary needs of Alaskaville will

also change as the community grows and future events

develop. Regardless, the impact of the millage rate cap

will have notable impacts to Alaskaville. How that impact

might be addressed by the community can take various

forms.

StateAssessor

58

Thank you for your time

and attention!

ANY QUESTIONS?

KatherineEldemar,DivisionDirector

katherine.eldemar@alaska.gov

MartyMcGee,StateAssessor

(907)269‐4605

Marty.mcg[email protected]

StateAssessorwebsite:

https://www.commerce.alaska.gov/web/dcra/OfficeoftheStateAssessor.aspx

DivisionofCommunityandRegionalAffairs

59